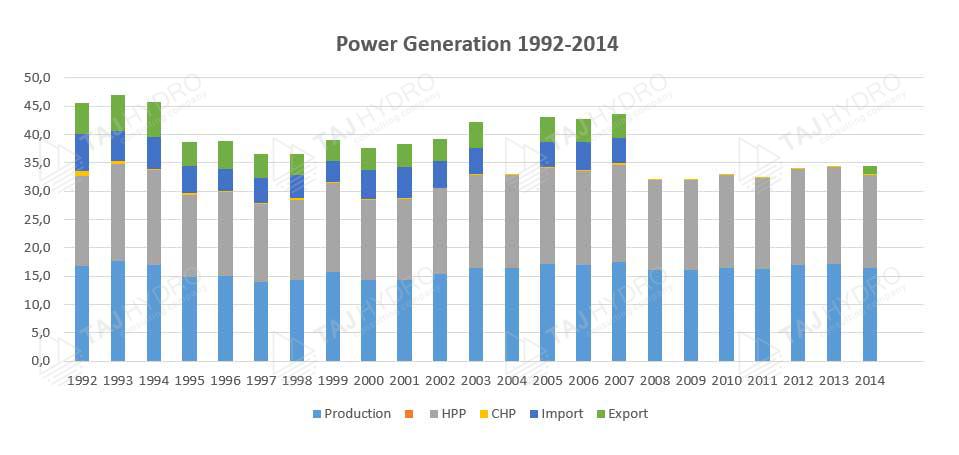

Tajikistan’s energy trade with the countries of the Central Asia Power System (CAPS) is currently very low. Energy trade continued immediately after the dissolution of the Soviet Union when, at the highest level, the countries established the Council to manage the operation of CAPS, supported by the Central Coordinating Dispatch Centre in Tashkent. However, in early 2000, after the significant increase in oil and gas prices, the previously agreed arrangement started crumbling. The last nail was Uzbekistan’s decision to disconnect Tajikistan from CAPS, which significantly curtailed opportunities for Tajikistan for its exports in summers as well as imports during winters, when it experiences serious shortfalls in supply. The current level of trade between the Central Asian countries is quite low and mostly dominated by Kyrgyz exports to Kazakhstan in summers to facilitate water for irrigation demand. There have been some exceptions to this, including recent Tajik exports to Kyrgyzstan to help them conserve water for winter demand, given the low inflows; exports by Kyrgyzstan to Uzbekistan in 2012-13 and by Uzbekistan to Tajikistan during the 2010 and 2011 winters.

The CAPS lacks mechanisms to monitor, discipline, and manage power flows. Price-based markets are in their infancy, and concepts that enhance trade benefits, such as time-of day pricing, value of ancillary services, and requirements for reserve margins are not integrated into investment or operations planning. There are also commercial concerns, including uncontrolled power flows, poor payment discipline, and uncoordinated pricing. These difficulties are overlaid with a political reluctance to engage in open trade.

All the countries are now attempting to become energy independent, but do recognize the value of trade to maximize benefits for themselves. The ADB and World Bank directly and through the Central Asia Regional Economic Cooperation (CAREC) are helping countries to find opportunities for increasing trade. In the absence of trade, Tajik and, to some extent, Kyrgyz investments for winter become uneconomical, as the capital cost needs to be amortised over less than six months, instead of full year supply. The ramifications of lack of summer exports are evident from very low utilization of hydro-based IPPs Sangtuda 1 and 2 and the build-up of outstanding debts. The CASA-1000 project, supported by several development partners, including the European Investment Bank, would help solve this issue for the existing capacity by connecting excess summer hydropower electricity from Tajikistan and Kyrgyzstan with markets in Afghanistan and Pakistan.

Currently Tajikistan has a power purchase agreement with Afghanistan for the supply of energy during summer from Sangtuda HPP to Kunduz substation via a double circuit 200 kV line with a capacity of 300 MW. The exports, which are limited mainly to summers, are increasing in quantum, but due to transmission and distribution constraints in Afghanistan, will continue around the same level in the medium term.